How The Petrodollar Quietly Died, And Nobody Noticed

By Tyler Durden

Two years ago, in hushed tones at first, then ever louder, the financial world began discussing that which shall never be discussed in polite company – the end of the system that according to many has framed and facilitated the US Dollar’s reserve currency status: the Petrodollar, or the world in which oil export countries would recycle the dollars they received in exchange for their oil exports, by purchasing more USD-denominated assets, boosting the financial strength of the reserve currency, leading to even higher asset prices and even more USD-denominated purchases, and so forth, in a virtuous (especially if one held US-denominated assets and printed US currency) loop.

The main thrust for this shift away from the USD, if primarily in the non-mainstream media, was that with Russia and China, as well as the rest of the BRIC nations, increasingly seeking to distance themselves from the US-led, “developed world” status quo spearheaded by the IMF, global trade would increasingly take place through bilateral arrangements which bypass the (Petro)dollar entirely. And sure enough, this has certainly been taking place, as first Russia and China, together with Iran, and ever more developing nations, have transacted among each other, bypassing the USD entirely, instead engaging in bilateral trade arrangements, leading to, among other thing, such discussions as, in today’s FT, why China’s Renminbi offshore market has gone from nothing to billions in a short space of time.

And yet, few would have believed that the Petrodollar did indeed quietly die, although ironically, without much input from either Russia or China, and paradoxically, mostly as a result of the actions of none other than the Fed itself, with its strong dollar policy, and to a lesser extent Saudi Arabia too, which by glutting the world with crude, first intended to crush Putin, and subsequently, to take out the US crude cost-curve, may have Plaxico’ed both itself, and its closest Petrodollar trading partner, the US of A.

As Reuters reports, for the first time in almost two decades, energy-exporting countries are set to pull their “petrodollars” out of world markets this year, citing a study by BNP Paribas (more details below). Basically, the Petrodollar, long serving as the US leverage to encourage and facilitate USD recycling, and a steady reinvestment in US-denominated assets by the Oil exporting nations, and thus a means to steadily increase the nominal price of all USD-priced assets, just drove itself into irrelevance.

A consequence of this year’s dramatic drop in oil prices, the shift is likely to cause global market liquidity to fall, the study showed.

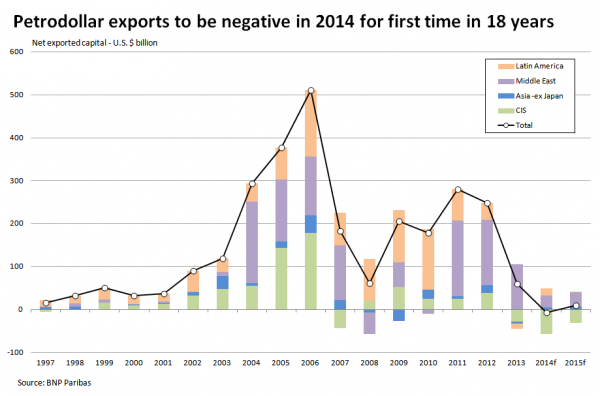

This decline follows years of windfalls for oil exporters such as Russia, Angola, Saudi Arabia and Nigeria. Much of that money found its way into financial markets, helping to boost asset prices and keep the cost of borrowing down, through so-called petrodollar recycling.

But no more: “this year the oil producers will effectively import capital amounting to $7.6 billion. By comparison, they exported $60 billion in 2013 and $248 billion in 2012, according to the following graphic based on BNP Paribas calculations.”

In short, the Petrodollar may not have died per se, at least not yet since the USD is still holding on to the reserve currency title if only for just a little longer, but it has managed to price itself into irrelevance, which from a USD-recycling standpoint, is essentially the same thing.

In short, the Petrodollar may not have died per se, at least not yet since the USD is still holding on to the reserve currency title if only for just a little longer, but it has managed to price itself into irrelevance, which from a USD-recycling standpoint, is essentially the same thing.

According to BNP, Petrodollar recycling peaked at $511 billion in 2006, or just about the time crude prices were preparing to go to $200, per Goldman Sachs. It is also the time when capital markets hit all time highs, only without the artificial crutches of every single central bank propping up the S&P ponzi house of cards on a daily basis. What happened after is known to all…

“At its peak, about $500 billion a year was being recycled back into financial markets. This will be the first year in a long time that energy exporters will be sucking capital out,” said David Spegel, global head of emerging market sovereign and corporate Research at BNP.

Spegel acknowledged that the net withdrawal was small. But he added: “What is interesting is they are draining rather than providing capital that is moving global liquidity. If oil prices fall further in coming years, energy producers will need more capital even if just to repay bonds.”

In other words, oil exporters are now pulling liquidity out of financial markets rather than putting money in. That could result in higher borrowing costs for governments, companies, and ultimately, consumers as money becomes scarcer.