The Aftermath Of The Great 2014 Oil Crash “A Textbook Macroeconomic Shock”

By Tyler Durden | Zero Hedge

Not a day passes without pundits on either side of the debate, eager to make their case that the acute, nearly 50% plunge in the price of crude, swear up and down their preferred economic ideology of choice that said plunge is [bullish|bearish] for the economy. The reality is that the true impact of the great oil crash of 2014 will not be revealed for at least several months, however for those who can’t afford to wait, or simply lack the patience, here is perhaps the most comprehensive view of the pros and cons of what has now been dubbed a “textbook macroeconomic shock” by Deutsche Bank.

From Deutsche Bank’s 2015 Credit Outlook titled “Plate Spinning”

The Great 2014 Oil Shock – Aftermath

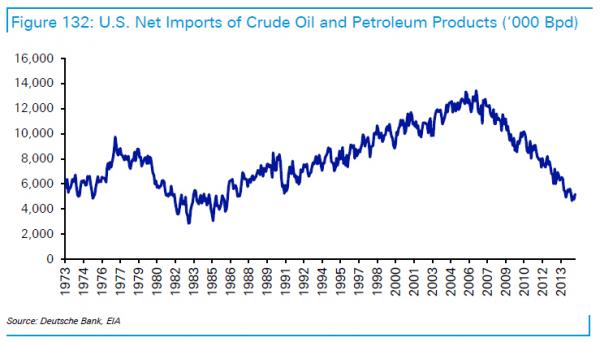

The fall in the price of oil – down more than 40% since June – is a textbook macroeconomic “shock”. Stripping it down to its most fundamental level, a fall in the price of oil predistributes real income from oil producers to oil consumers. Money oil consumers would have exchanged with oil producers for the stuff, can instead be put towards other purchases or savings. At the global level it means less spent on oil imports for oil importing nations and less income from oil exports for oil exporting nations. To put some rough numbers around this, US average net imports of oil and the like has averaged 5.2m barrels per day in 2014, thus the fall in the oil price by $43 since late June is saving the US economy about $224m a day on its net oil transactions and costing its oil trade partners the same amount. This is after accounting for the dramatic fall in US net oil imports driven in part by the country’s shale boom.

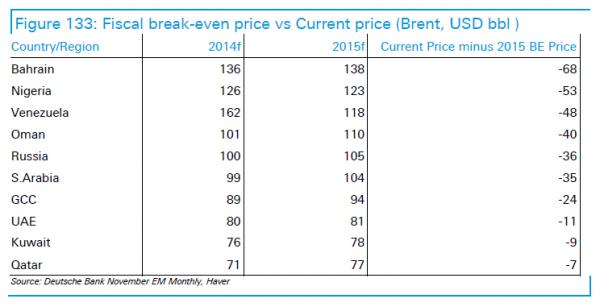

Therefore if oil prices stay where they currently are this appears to be a meaningful headwind for the big oil consuming nations. The biggest net oil importers in 2013 were (1) the US, (2) China, (3) Japan and (4) India. Major exporters will suffer. Probably the most prominent current example of an economy that will struggle to cope with the fall in the oil price is Russia, which in 2013 was the world’s second largest net exporter of oil. As we’ve already discussed, estimates suggest that at oil prices below $90 the Russian economy will go into recession and DB estimates the government will fail to balance its budget at $100 (Figure 133). At current levels none of the major oil exporters will be able to balance their budgets next year.

Overall, most estimates suggest that a fall in the oil price is a net positive for the total world economy. According to the IMF’s Tom Helbling, “a 10% change in the oil price is associated with around a 0.2% change in global GDP” (The Economist) as oil consumers are greater spend-thrifts than oil producers. Given those estimates the current fall of more than 40% should add about +0.8% to global GDP growth.

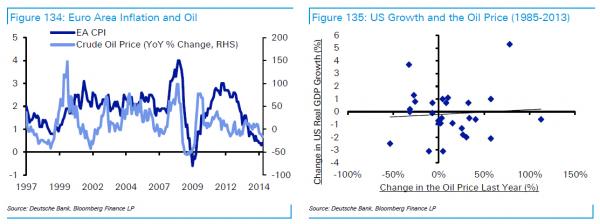

With so much of the global growth story resting on US shoulders next year the fall in the price of oil should help, although not as much as it used to given the USA’s shale boom. The EU should also gain given its $500bn of energy imports in 2013. However the drop in the price of oil might prove a mixed blessing given that sharp drops in the oil price will weigh on inflation (Figure 134) and another negative headwind to inflation (in any form) is not something the euro area really needs or wants currently with CPI running at just +0.4% YoY. On the other hand the drop in inflation pressures should be a boon for a number of EM economies whose central banks may otherwise have had to hike rates in the face of rising inflation even as their growth rates remained tepid.

It’s also important to remember that whilst oil is an important global commodity it is rare for it alone to drive global economic outcomes. The halving of global oil prices in 2008 didn’t prevent many of the world’s oil importing economies from suffering severe recessions and as Figure 135 shows there is no easy nor automatic relationship between falling oil prices and rising US growth. The environment within which the oil price change occurs is important. Indeed if the current drop in the price of oil is being driven by expectations of falling demand driven by expectations of a slowdown in global growth it’s possible that the drop in the oil price is at best going to partially cushion the global economy from a slowdown rather then drive it to higher growth rates.

Also importantly for investors, falling oil prices will not affect all areas of economies equally, even in those economies that should benefit at an aggregate level. As our US credit strategy team wrote recently, energy companies make up the largest single sector component of the US HY market at 16% (US HY DM Index) and so the falling oil price may prove a negative for the US HY credit market. Our US team added that if the WTI price fell to $60/bbl this would push the whole US HY energy sector into distress, with around 1/3rd of US energy Bs/CCCs forced to restructure, implying a 15% default rate for overall US HY energy which would contribute 2.5% to the broad US HY default rate. This could be a sizeable enough shock to cause concern throughout the rest of the US HY market.

There is no doubt that the fall in the price of oil in 2014 has been a significant economic shock. Most estimates suggest that this should add to global growth, weigh on global inflation and most likely have varied but oil-specific asset price implications (EM oil producing nations and US HY weakness stand out); however it is likely that growth tailwinds from this year’s fall in oil prices will not be the main story for investors in 2015.