JPMorgan’s 5 Reasons To Sell USA & Buy Europe

By Tyler Durden | ZeroHedge

JPMorgan Cazenove’s global equity strategy group has decided enough is enough – the underperformance of the Eurozone is getting stretched (they note), and are upgrading Euro equity allocations to Overweight at the expense of an Underweight in US stocks. Here are the fives reasons why they made the shift…

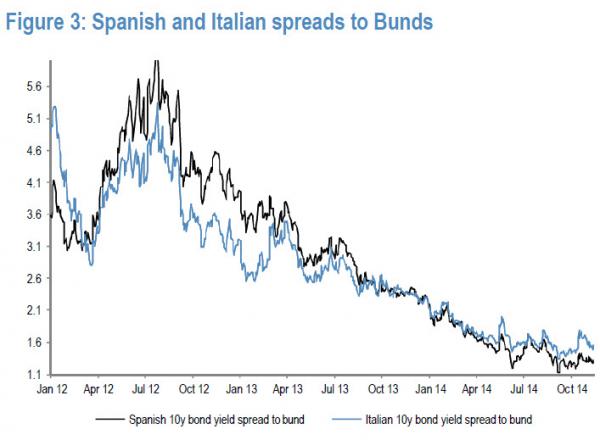

1) Eurozone has posted an exceptionally poor performance ytd, lagging the US by 22% in USD terms. It is now trading at a lower price relative than the one recorded at the point of peak stress in ’12, when Eurozone breakup was almost the base case.

In contrast to record wide peripheral spreads seen in ‘12, these are nowadays well behaved, at a tight 130bp,

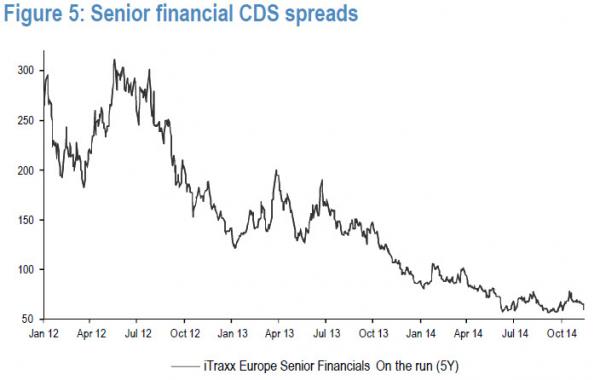

and financial CDS spreads are at a healthy 65bp.

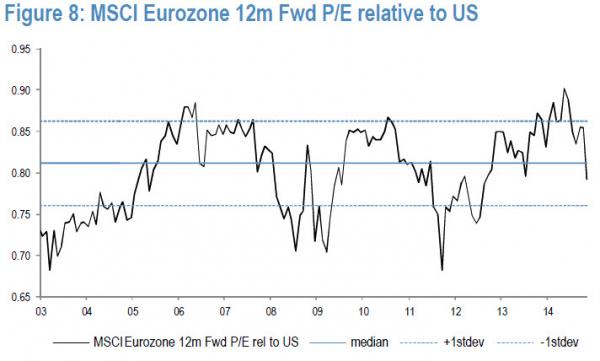

2) Forward P/E relative of Eurozone has improved substantially. Eurozone traded at record expensive levels earlier in the year, but has moved to the cheap side of fair value now.

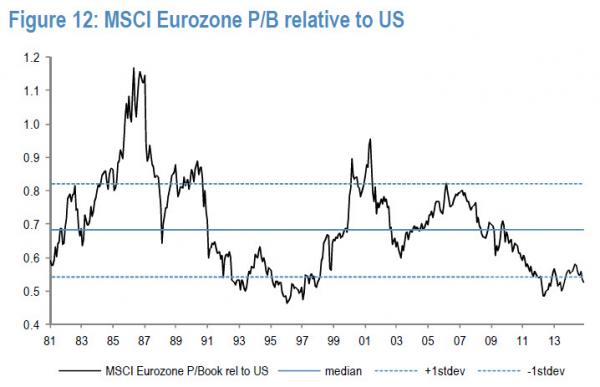

The longer-term metrics, such as Shiller P/E and P/B, remain supportive of Eurozone.

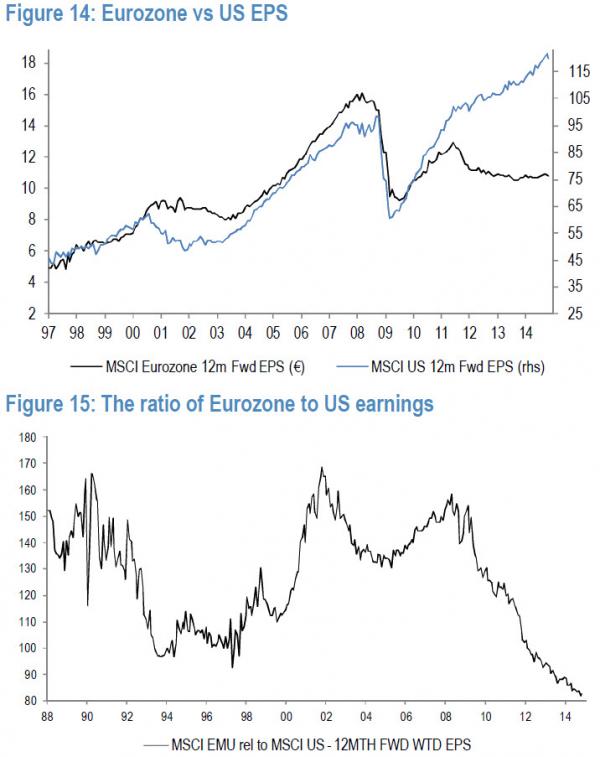

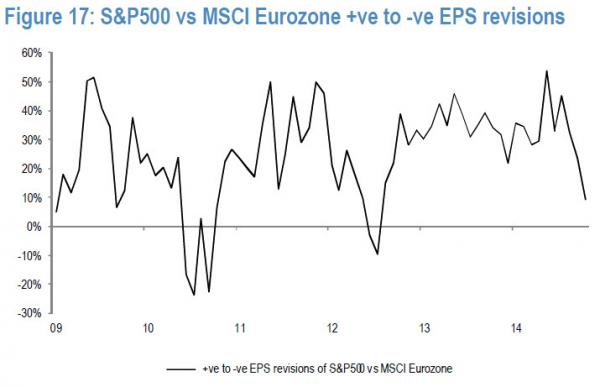

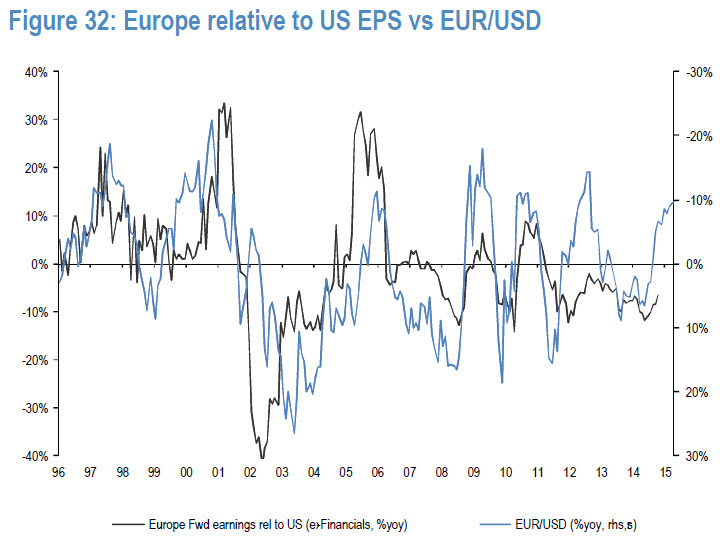

3) The level of Eurozone earnings relative to the US has never been as depressed as it is today.

The ROE differential between the two regions is at the top of its historical range, and it should start to normalise from here. We note that the EPS revisions in the US are not much better than those in Eurozone anymore – the gap is closing.

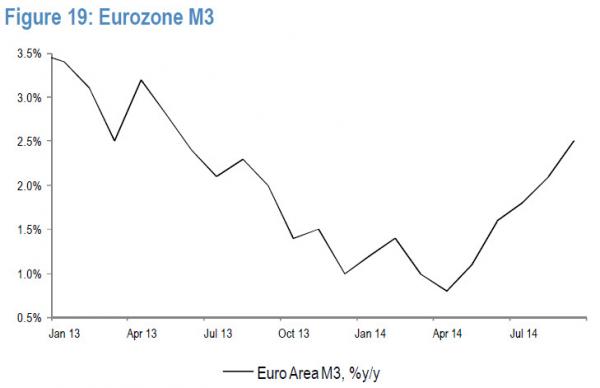

4) Eurozone M3 has been picking up since April and it tends to lead economic activity. The credit cycle appears to be bottoming out in the region – there is a clear 2nd derivative visible in Spain and Italy.

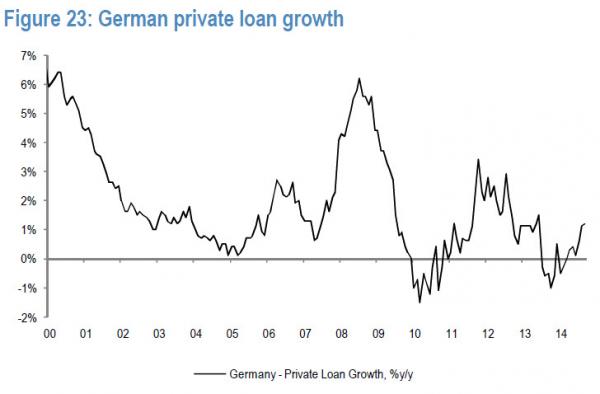

German loan growth has already turned outright positive.

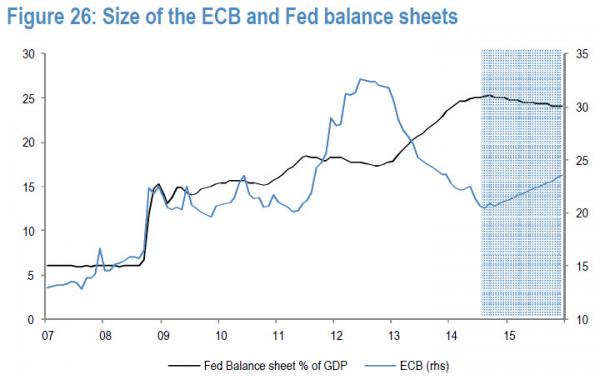

Three quarters of all financing in Europe is done through banks, so the fact that stress tests are finally behind us should allow the banks to be more supportive of the economy. The takeup in December T-LTRO could be more favourable than the previous one. ECB balance sheet will expand by 35% from here, we expect, which is not negligible. In contrast, US money printing is done.

5) Falling Euro is a tailwind for growth, for exporters and for earnings. Our economists suggest a 10% move lower in the trade-weighted Euro should boost growth by 1% over a two-three year period.

* * *

We see this as a relative call, where we believe Eurozone is due a period of outperformance vs the US, but continue to expect US stocks to make new highs in absolute terms. We stay UW the UK and OW Japan in the global portfolio.